EFAMA, BFPI Ireland, EACB, FIA EPTA, Federation of the Dutch Pension Funds,

Finance Denmark, Nordic Securities Association, AIMA, ICI Global, FIA and ISDA support positive

incentives to further enhance the attractiveness of EU clearing and EU Capital Markets, including

many of the measures proposed in EMIR 3.0. (read more)

European Market Infrastructures regulation (EMIR)

In 2012, following the 2008 financial crisis, the EU adopted the European Market Infrastructures regulation (EMIR) with the laudable objectives of increasing transparency in the OTC derivatives markets, to reduce the counterparty risk of derivatives contracts and to reduce operational risks associated with derivatives trading.

EFAMA welcomes the improvements recently brought by the EMIR Refit: It redefines the obligations imposed on derivatives users, recognising and solving some issues previously existing in EMIR, such as the disproportionate regulatory burden imposed on the least risky counterparties. We also advocate for a better alignment between EMIR and MiFIR, especially with regards to the clearing and trading obligations.

Related policy positions

Policy Position

EMIR

07 September 2023

Active Accounts - Joint Trade Association Statement

Policy Position

EMIR

19 June 2023

EMIR 3.0: Detailed views on active accounts

EFAMA offers a detailed view on the active accounts proposal in this paper. Costs to the end investor are broken down into two main buckets i) operational build-out and ii) in nominal terms the much larger impact of loss of netting efficiencies. Potential impacts on financial stability are also examined, with a focus on the widening basis which will result from large volumes of one-directional flows onto an EU-CCP. The impact on margins and procyclicality are also studied. The analysis points to increased liquidity risk for

Policy Position

EMIR

21 March 2023

Mandated levels of EU Clearing run counter to competitive and efficient clearing systems

EFAMA appreciates the opportunity to comment on the EMIR 3.0 proposal reforming the clearing framework in the EU. We share the objectives of this review which seek to ensure financial stability in the EU, and the well-functioning of the existing central clearing framework. We understand the objective to reduce excessive exposure to substantially systemic CCPs over time, though we maintain that any regulatory measures should be proportionate to the regulatory rationale, and should not unduly harm market participants.

Related news

Policy Position

Capital Markets

EMIR

08 April 2022

EFAMA views and recommendations on ESMA's consultation on the review of EMIR RTS on APC margin measures

The European Fund and Asset Management Association (EFAMA) welcomes the opportunity to respond to this important review of RTS 153/2013 and accompanying guidelines, in light of the procyclicality witnessed during the peak volatility of the Covid crisis. European CCPs already have standard anti-procyclicality tools in their rulebooks and this did lead to less volatile moves in margin in Europe versus other jurisdictions.

Press Release

Capital Markets

EMIR

MIFID

Capital Markets Union

Data

07 October 2021

Statement on the release of the Oliver Wyman study ‘Caught on Tape’

“Oliver Wyman’s study ‘Caught on Tape’ provides a perplexing take on Consolidated Tape for Europe. Sure enough, it starts with accurate observations: the high number of trading venues in Europe, the resultant fragmented liquidity, unseen liquidity due to the lack of a consolidated tape, and the fact that leading markets like the US and Canada today benefit from a real time consolidated tape.

Infographic

Capital Markets

EMIR

MIFID

Data

06 October 2021

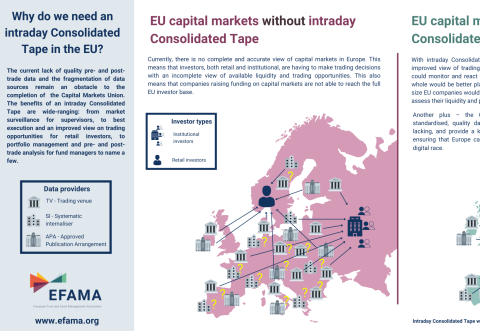

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Related publications

Infographic

Capital Markets

EMIR

MIFID

Data

06 October 2021

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Contact

Deputy Director, Capital Markets and Digital