EFAMA has some concerns with ESMA’s clarifications. In the consultation paper (CP), ESMA seems to have a very broad interpretation of the ‘multilateral systems’ definition under MiFID II and states that ‘systems where trading interests can interact but where the execution of transactions is formally undertaken outside the system still qualify as a multilateral system and should be required to seek authorisation’ (paragraph 36).

MiFID / MiFIR

The Markets in Financial Instruments Directive (MiFID) is a cornerstone of EU financial services legislation and is of direct relevance to asset management companies. In 2014, the European Commission adopted new rules revising MiFID, consisting of a Directive (MiFID II) and a regulation (MiFIR). Overall, MiFID II yielded positive results in terms of liquidity and transparency for investors.

Among possible improvements to the MiFID framework, EFAMA encourages the creation of a well-structured, reasonably priced consolidated tape managed by ESMA and fed by all trading venues and systematic internalisers for all financial instruments. A second, long-term EFAMA objective is better enforcement of data providers’ existing obligation to provide market data on a “reasonable commercial basis”.

Related policy positions

Policy position

25 November 2020

EFAMA's reply to ESMA's CP on MiFID II / MiFIR review on the functioning of Organised Trading Facilities (OTF)

Policy position

Capital Markets

Distribution & Client Disclosures

EU Fund regulation

UCITS

23 November 2020

EFAMA's reply to ESMA's CP on MiFIR Review report on the obligations to report transactions & reference data

We disagree with an extension of its scope to UCITS’ and AIFs’ management companies to the scope of the reporting requirements imposed by MiFIR, Art. 26. This extension would be in breach of the principle of proportionality, as:

Policy position

Capital Markets

14 September 2020

EFAMA comments EC CP on a Covid-19 Capital Markets Recovery Package

EFAMA appreciates the Commission's efforts in pursuing an alleviation of certain MiFID II requirements in the interest of promoting a swift recovery from the economic crisis precipitated by the Covid-19 pandemic (....).

EFAMA believes however that there are more effective ways to foster SME access to markets and urges the Commission to consider a set of further measures (...)

Related news

Press Release

17 January 2023

MiFIDII/MiFIR review will be key to the future success and competitiveness of the EU’s capital markets

The ongoing review of MiFIDII/MiFIR is an important moment for the future success of the Capital Markets Union project. The European Council adopted their position at the end of last year and the European Parliament is currently debating these future rules, with the expectation of a draft report by the end of the month.

Policy Position

17 January 2023

MiFIDII/ MiFIR review - EFAMA-BVI-EFSA-NSA priorities

The MiFID/MiFIR review will be key to the future success and competitiveness of the EU's capital markets.

With international competition for investment heating up markedly, European legislators need to ensure that EU regulation is helping, and not hindering, capital market growth and participation.

Various European trade associations representing EU capital markets, including EFAMA, BVI, EFSA and NSA, have published a letter outlining their main priorities for the review. This includes the following core elements:

Press Release

29 November 2022

The availability of a real-time consolidated tape in Europe is critical for the success of the CMU

EFAMA members are paying close attention to the ongoing discussions in the European Parliament and Council to reach a compromise on the MiFID review. Together with a broad majority of market participants, including the sell-side and alternative trading venues, we have consistently made the case for a real-time tape for equities with the inclusion of pre and post-trade data.

Related publications

Publication

Capital Markets

MIFID

16 November 2021

Buy-side use-cases for a real-time consolidated tape

A real-time consolidated tape, provided it is made available at a reasonable cost, will bring many benefits to European capital markets. A complete and consistent view of market-wide prices and trading volumes is necessary for any market, though this is especially true for the EU where trading is fragmented across a large number of trading venues. A real-time consolidated tape should cover equities and bonds, delivering data in ‘as close to real-time as technically possible’ after receipt of the data from the different trade venues.

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

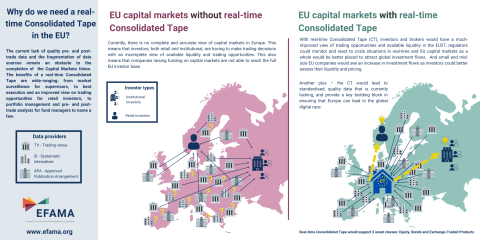

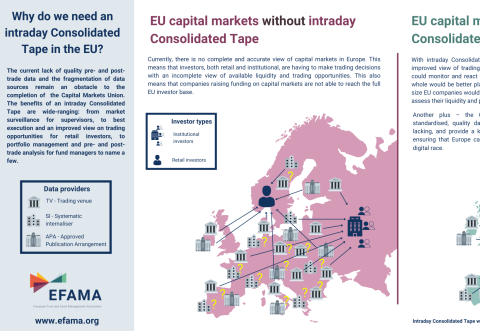

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Publication

MIFID

Distribution & Client Disclosures

PRIIPs

Management Companies

AIFMD

03 June 2020

Investment Funds Distributor Due Diligence Questionnaire

Funds face unique challenges in performing intermediary oversight, and especially so because of MiFID II requirements, changing regulatory landscapes, and the absence of an industry agreed-upon standard between funds and their distribution channels. To help address these challenges, a dedicated working group developed a uniform due diligence questionnaire (DDQ) that will serve as the standard for investment funds (UCITS and AIFs) in performing onboarding and ongoing oversight of distribution channels.