List of recommendations show what is needed to ensure a successful tape.

The Markets in Financial Instruments Directive (MiFID) is a cornerstone of EU financial services legislation and is of direct relevance to asset management companies. In 2014, the European Commission adopted new rules revising MiFID, consisting of a Directive (MiFID II) and a regulation (MiFIR). Overall, MiFID II yielded positive results in terms of liquidity and transparency for investors.

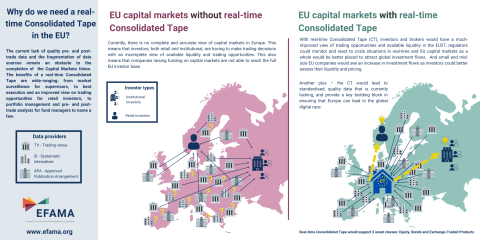

Among possible improvements to the MiFID framework, EFAMA encourages the creation of a well-structured, reasonably priced consolidated tape managed by ESMA and fed by all trading venues and systematic internalisers for all financial instruments. A second, long-term EFAMA objective is better enforcement of data providers’ existing obligation to provide market data on a “reasonable commercial basis”.

List of recommendations show what is needed to ensure a successful tape.

The FCA’s recent report on the wholesale data market is an important and high-quality study which echoes many long-standing buy-side concerns. It finds evidence of unequal market power in terms of market concentration, highly profitable margins, opaque pricing practices, excessive charging, bundling practices and complex licensing agreements, all of which negatively impact data users. Much of this data is indispensable for users to stay in business and fulfil regulatory obligations.

EU asset managers, banks and brokers are today urging policy makers not to concede to pressure which will lead to suboptimal outcomes in the review of the Markets in Financial Instruments Directive (MiFID/R).

Funds face unique challenges in performing intermediary oversight, and especially so because of MiFID II requirements, changing regulatory landscapes, and the absence of an industry agreed-upon standard between funds and their distribution channels. To help address these challenges, a dedicated working group developed a uniform due diligence questionnaire (DDQ) that will serve as the standard for investment funds (UCITS and AIFs) in performing onboarding and ongoing oversight of distribution channels.

EFAMA has submitted its  response to the European Commission's consultations on the review of the MIFID II / MIFIR regulatory framework, where it has outlined its recommendations on investor protection and capital markets and infrastructure.

response to the European Commission's consultations on the review of the MIFID II / MIFIR regulatory framework, where it has outlined its recommendations on investor protection and capital markets and infrastructure.

EFAMA's Director General Tanguy van de Werve commented: