European Market Infrastructures regulation (EMIR)

In 2012, following the 2008 financial crisis, the EU adopted the European Market Infrastructures regulation (EMIR) with the laudable objectives of increasing transparency in the OTC derivatives markets, to reduce the counterparty risk of derivatives contracts and to reduce operational risks associated with derivatives trading.

EFAMA welcomes the improvements recently brought by the EMIR Refit: It redefines the obligations imposed on derivatives users, recognising and solving some issues previously existing in EMIR, such as the disproportionate regulatory burden imposed on the least risky counterparties. We also advocate for a better alignment between EMIR and MiFIR, especially with regards to the clearing and trading obligations.

EFAMA's reply to ESMA's consultation paper on the Alignement of MiFIR with the changes introduced by EMIR Refit

Joint associations letter on Temporary Equivalence and Recognition in relation to UK CCPs

EFAMA reply to FSB consultation on Incentives to Centrally Clear over-the-Counter (OTC) Derivatives

Mandated levels of EU Clearing run counter to competitive and efficient clearing systems

EFAMA appreciates the opportunity to comment on the EMIR 3.0 proposal reforming the clearing framework in the EU. We share the objectives of this review which seek to ensure financial stability in the EU, and the well-functioning of the existing central clearing framework. We understand the objective to reduce excessive exposure to substantially systemic CCPs over time, though we maintain that any regulatory measures should be proportionate to the regulatory rationale, and should not unduly harm market participants.

Mandated levels of EU Clearing run counter to competitive and efficient clearing systems

EFAMA has today published its response to the European Commission’s EMIR 3.0 proposal. We support the EC’s goal of increasing the attractiveness of EU central clearing counterparties (CCPs), including simplified product approvals, faster model change authorisations, and greater margin model transparency. A new clearing threshold calculation is also proposed, which further aligns the Clearing Obligation with the rest of the EMIR regulation.

ISDA, AIMA, EFAMA, FIA Statement on European Commission's Proposed Amendments to EMIR

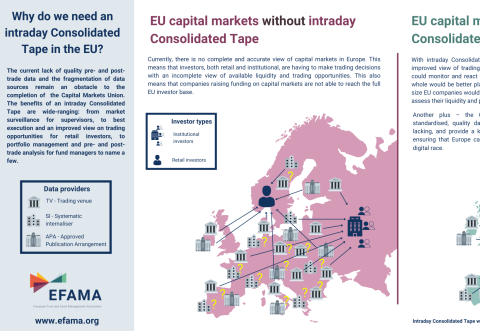

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.