European Market Infrastructures regulation (EMIR)

In 2012, following the 2008 financial crisis, the EU adopted the European Market Infrastructures regulation (EMIR) with the laudable objectives of increasing transparency in the OTC derivatives markets, to reduce the counterparty risk of derivatives contracts and to reduce operational risks associated with derivatives trading.

EFAMA welcomes the improvements recently brought by the EMIR Refit: It redefines the obligations imposed on derivatives users, recognising and solving some issues previously existing in EMIR, such as the disproportionate regulatory burden imposed on the least risky counterparties. We also advocate for a better alignment between EMIR and MiFIR, especially with regards to the clearing and trading obligations.

Industry Association Letter on Impact of COVID-19 on Initial Margin Phase-In

EFAMA Reply: ESMA CP on review report MiFIR transparency regime for equity, ETFs & other related instruments

EFAMA's reply to ESMA's CP on Draft technical advice on commercial terms for providing clearing services under EMIR (FRANDT)

UK clearing house equivalence - request from nine trade associations

Nine associations (AFME, AIMA, EAPB, EBF, EFAMA, FIA, ICI, ISDA, SIFMA AMG) welcome the Commission's decision to grant a time-limited equivalence decision in respect of UK CCPs. However, when this time-limited equivalence decision expires on 30 June 2022, there remains a significant risk of disruption to clearing for EU firms and to their access to global markets.

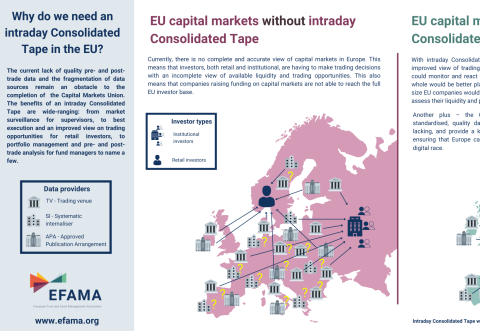

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.