We see great value in the creation of a consolidated tape to support Europe’s capital markets. However, we qualify that statement with a reminder that the framework for a successful consolidated tape should

i) address the known market failure around market data costs,

ii) manage the costs of the tape by limiting compensation for data contributors to the cost of production,

iii) simplify transparency requirements without harming the balance between transparency and liquidity, and

iv) support rather than limit competition between execution venues as introduced with MiFID I and MiFID/MiFIR.

We would also like to emphasise that several of the reform proposals for both equities and non-equities transparency regimes are based on expected benefits that have not been subjected to much needed in-depth analysis, and a comprehensive impact assessment.

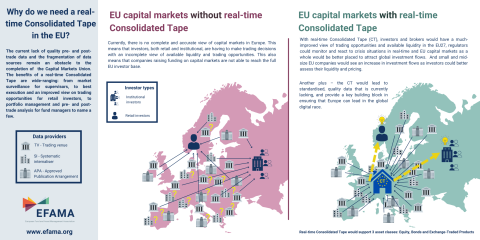

A Consolidated Tape will help bridge European capital markets

EFSA and EFAMA[1], as representatives of the buy and sell-side communities in the EU, were pleased to see an ambitious push from the Commission last week to put in a place a consolidated tape (CT) for market data. We support the principles of mandatory contribution and voluntary consumption of the CT, which we consider crucial for the sell and buy-side communities. Moreover, we believe that it should be possible to have granular consumption; that is to receive the data from a chosen number of trading venues, APAs or SIs as is currently the case. We also want to stress that the establishment of CTs should not result in changes to the EU’s best execution framework which functions well today and would suffer from added complexity.

However, level-playing-field when compensating data contributors must be a focus

We are concerned about a model which puts ‘fair remuneration of data contributors’ as a key feature enabling an equities CT. Furthermore, we consider the proposal to compensate the data contributors through ‘minimum revenue targets’ as currently defined to be open-ended with no visible ceiling capping costs to a level associated with the actual production of data. We call for the revenue sharing scheme to be more precisely defined and extended to all contributors beyond regulated markets. Notably, it should specify the constitution of the total amount to be redistributed, to ensure that contributors have a stake in the success of the tape and that subscription to the tape remains attractive for market participants. As we have pointed out elsewhere[2], the MiFIR Level 1 text should reflect that market data should be provided on the basis of costs and that trading venues, APAs, SIs and CTPs should disclose relevant information in this area to National Competent Authorities (NCAs).

When considering the sharing of revenues generated by a consolidated tape, it is important to remember that trading venues (in particular incumbent exchanges) will continue to collect revenue from both proprietary data and the new CT as their proprietary data will continue to be indispensable for investment firms.

And market data cost must be addressed whether there is a CT or not

Market data costs must be addressed independently of the CT. We recognise that the Commission proposal includes ESMA’s recommendation to convert the ESMA guidelines on market data into legal text as well as the the empowerment of ESMA to specify how RCB should be applied by further strengthening the application of Article 13, MiFIR. However, a number of ESMA’s remaining recommendations are unfortunately not included in the proposal.[3] This includes the ESMA recommendation to move the provision to provide market data on the basis of costs to the Level 1 text, and the deletion of the articles allowing trading venues, APAs, CTPs and SIs to charge for market data proportionate to the value the market data represents to users. This contradicts the cost-based approach.

Nor should a CT compromise the delicate balance between transparency and liquidity for non-equity markets

As far as the trade transparency aspects of the proposal (especially for bonds), we are not opposed to the simplification of the current regime provided that it is aligned with the current rules that enable adequate deferral of publication. Nevertheless, the proposals do not ensure a deferral regime calibrated in a way which enables SIs and other liquidity providers to unwind their risks. The balance between transparency and liquidity is delicate: If SIs and other liquidity providers are exposed to undue risks from too much transparency, they could either withdraw or widen spreads to protect themselves. This will result in reduced liquidity, which harms clients and, ultimately, end-investors. Moreover, there is a strong risk that it would have a detrimental impact on the attractiveness of EU markets compared to other markets which might have a greater ability and willingness to provide liquidity. We are concerned with the deletion of both pre- and post-SSTI without clear expectations as to the availability of alternatives given the limited possibilities to defer prices. There appears to be no possibility to defer price disclosure beyond End of Day for transactions that are large in scale or in illiquid instruments. This will ultimately harm asset managers’ ability to fulfil their fiduciary duty toward end-clients on best execution.

Competition between execution venues must be encouraged, not distorted

For equities in particular, we note several attempts to direct flow to Regulated Markets at the expense of other execution venues. Equity market structure changes such as those contained in the EC’s recent proposals, create an unlevel field and compromise competition introduced with MiFID I. Such step is damaging for clients’ choices and to the competitive and diverse nature of the EU’s trading landscape.

Repeal of additional, unnecessary EU reporting

We strongly applaud the decision by the EC to repeal the RTS 27 “Best Execution” Reports.

However, and as already regularly requested since the implementation of MiFID several years ago, we think that this repeal of RTS 27 “Best Execution” Reports should be accompanied by the repeal of RTS 28 “Best Execution” Reports.

We have stressed and continue to stress the significant costs of producing these reports for which there appears to be very little demand. Professional end-investors already have access to proprietary tools and data for assessing best execution. The multiple asset class consolidated tape referenced above will provide valuable data toward retails investors for their best execution needs.

Finally, it seems unfair and punitive to require EU firms to maintain publication of RTS28 reports when other jurisdictions have removed such requirements. [4]

We therefore respectfully request the EC to consider removing the RTS 28 ‘Best Execution’ Report obligation.

[1] EFAMA,the voice of the European investment management industry, represents 28 Member Associations, 60 Corporate Members and 24 Associate Members. At end Q2 2020, total net assets of European investment funds reached EUR 17.1 trillion. These assets were managed by almost 34,200 UCITS (Undertakings for Collective Investments in Transferable Securities) and more than 29,100 AIFs (Alternative Investment Funds). More information is available at www.efama.org. EFSA is a forum of European Securities Associations gathering the Association for Financial Markets in Europe (AFME), the French Association of Financial Markets (AMAFI), the Spanish Asociación de Mercados Financieros (AMF), the Italian Association of Financial Intermediaries (ASSOSIM), the Danish Securities Dealers Association (DSDA), The German Federal Association of Securities Trading Firms (bwf), The Belgian Financial Sector Federation (Febelfin), The Polish Securities Dealers Association (IDM) and the Swedish Securities Markets Association (SSMA).

[2] Please see our recommendations as published by EFAMA here and EFSA here

[3] ESMA Final Report on market data costs point 58-65, page 26-27.

[4] https://www.fca.org.uk/publications/policy-statements/ps21-20-changes-uk-mifids-conduct-and-organisational-requirements