EFAMA replied to a specific question on moving to stage 3 for the determination of the liquidity assessment of bonds.

Capital markets

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

Related policy positions

Policy position

Capital Markets

MIFID

Distribution & Client Disclosures

11 June 2021

MiFID: EFAMA replies to ESMA consultation on RTS 2 Annual Review

Policy position

Capital Markets

MIFID

Distribution & Client Disclosures

29 April 2021

ESMA consults on guidelines of the MIFID II appropriateness and execution-only requirements

EFAMA agrees in principle with many of ESMA’s suggested approaches in their consultation on guidelines on certain aspects of the MIFID II appropriateness and execution-only requirements. However, certain, essential elements still require further considerations before finalising these Guidelines.

Policy Position

Capital Markets

CSDR

12 March 2021

Joint trade association letter regarding Implementation of CSDR SDR

On 11 March 2021, EFAMA and 14 trade associations representing a wide range of stakeholders in the European and global financial markets wrote to the European Commission and ESMA raising concerns about the implementation of the mandatory buy-in requirement under the EU’s CSDR Settlement Discipline Regime.

Related news

Press Release

Capital Markets

Data

04 February 2025

European Stock Exchanges' Over-Reliance on Equity Market Data Revenues: Stifling Growth and Innovation

Rising data fees to offset declining trading revenue burden market participants with surging costs

Policy Position

Capital Markets

EU Fund regulation

05 December 2024

EC Targeted consultation on the functioning of the EU securitisation framework

The EU Securitisation Regulation, which aimed to enhance transparency and strengthen trust, is undergoing a very timely review. EFAMA supports the European Commission’s initiative to engage stakeholders in shaping key improvements to this critical framework.

Press Release

Capital Markets

02 September 2024

Robust governance needed for future consolidated tape providers

ESMA technical standards move one step closer to consolidated tape launch.

ESMA recently closed the consultation for regulatory technical standards that will define the competitive selection process for the consolidated tape, as well as the technical abilities that applicants will be assessed on. In its response for the buy-side, EFAMA stressed that a robust governance framework for the operators of the tapes is critical.

Related publications

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

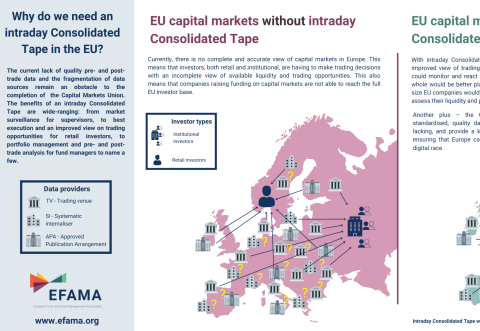

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Publication

Capital Markets

Benchmarks

06 July 2021

3 Questions to Jean-Louis Schirmann on the use of EURIBOR

Q #1 How was Euribor impacted by the adoption of the Benchmark Regulation (BMR) and what are the relevant features of the reformed Euribor for investment managers?

Publication

Capital Markets

Benchmarks

30 June 2021

3 Questions to Christophe Binet on LIBOR Transition

Q #1 When will LIBOR phase out and which rates will be replacing it?

The London Interbank Offered Rate, also known as LIBOR®, is a widely-used index for short-term interest rates that is commonly found in

Contact

Deputy Director, Capital Markets and Digital