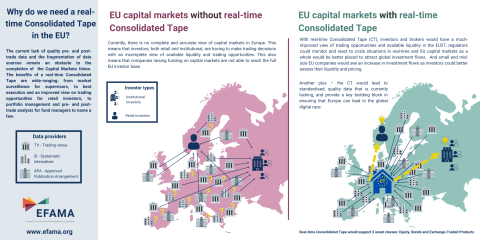

In a letter to policymakers, 18 European buy-side firms state that only an Equities/ETFs tape that delivers data in real-time and that includes pre-trade data in the form of 5 layers of best bid and offer, will meet with the necessary market demand to make the Equities/ETFs Consolidated Tape commercially viable. A reasonably priced tape is also a precondition for success, they argue.

MiFID / MiFIR

The Markets in Financial Instruments Directive (MiFID) is a cornerstone of EU financial services legislation and is of direct relevance to asset management companies. In 2014, the European Commission adopted new rules revising MiFID, consisting of a Directive (MiFID II) and a regulation (MiFIR). Overall, MiFID II yielded positive results in terms of liquidity and transparency for investors.

Among possible improvements to the MiFID framework, EFAMA encourages the creation of a well-structured, reasonably priced consolidated tape managed by ESMA and fed by all trading venues and systematic internalisers for all financial instruments. A second, long-term EFAMA objective is better enforcement of data providers’ existing obligation to provide market data on a “reasonable commercial basis”.

Related policy positions

Policy Position

14 April 2023

European asset managers in full support of the European Parliament's proposal on Equities Consolidated Tape

Policy Position

17 January 2023

MiFIDII/ MiFIR review - EFAMA-BVI-EFSA-NSA priorities

The MiFID/MiFIR review will be key to the future success and competitiveness of the EU's capital markets.

With international competition for investment heating up markedly, European legislators need to ensure that EU regulation is helping, and not hindering, capital market growth and participation.

Various European trade associations representing EU capital markets, including EFAMA, BVI, EFSA and NSA, have published a letter outlining their main priorities for the review. This includes the following core elements:

Policy Position

11 July 2022

EFAMA responses to the discussion questions within the IOSCO report “corporate bond markets – drivers of liquidity during covid-19 induced market stresses”

EFAMA is appreciative of the opportunity to comment on this major IOSCO study on the dynamics of bond market liquidity during market stresses. We provide some detailed responses below, but would reiterate a few high-level points here:

Related news

Policy Position

Capital Markets

MIFID

07 July 2021

Ensuring a market structure and a transparency regime which facilitate liquidity, investors’ choice, and funding of companies | Joint statement

Well-functioning and liquid capital markets are fostered by an efficient market structure and supporting legislative frameworks. A diverse and efficient market structure reduces the costs of trading whilst promoting best execution. This optimises funding opportunities for issuers and maximises returns for investors and savers.

Announcement

MIFID

Competitiveness

Distribution & Client Disclosures

15 February 2021

FinDatEx launches interim version of European MiFID Template

The Financial Data Exchange Templates (FinDatEx) platform today published an interim version of the European MiFID Template (EMT V3.1) which is available on the FinDatEx website. The purpose of this interim version is to answer the demand of product distributors and manufacturers to cope with the basic implementation of MiFID II ESG/SFDR principles, and in view of the misaligned application dates of SFDR Level 1, SFDR RTS and MiFID II delegated acts.

Announcement

MIFID

Distribution & Client Disclosures

01 December 2020

Financial Data Exchange Templates (FinDatEx) platform publishes European Feedback Template

Financial Data Exchange Templates (FinDatEx) platform published on 01 December 2020 the European Feedback Template (EFT V1). This template standardises the information to be sent back from the distributor to the manufacturer under the MiFID 2 target market requirements. This is the first European wide feedback template. The EFT and all other FinDatEx templates are not compulsory, provided to the industry free of charge and are free of any intellectual property rights.

Related publications

Publication

Capital Markets

MIFID

Data

Distribution & Client Disclosures

04 March 2020