EFAMA welcomes this opportunity to comment on the review of the provisions within the Short Selling Regulation. We have limited our responses to those questions of most relevance to our membership.

Capital markets

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

Related policy positions

Policy position

Capital Markets

19 November 2021

ESMA Consultation on the review of certain aspects of the short selling regulation

Policy Position

Capital Markets

EMIR

16 September 2021

UK clearing house equivalence - request from nine trade associations

Nine associations (AFME, AIMA, EAPB, EBF, EFAMA, FIA, ICI, ISDA, SIFMA AMG) welcome the Commission's decision to grant a time-limited equivalence decision in respect of UK CCPs. However, when this time-limited equivalence decision expires on 30 June 2022, there remains a significant risk of disruption to clearing for EU firms and to their access to global markets.

Policy Position

Capital Markets

CSDR

15 July 2021

Joint association letter on the CSDR Settlement Discipline implementation timeline

On 14 July 2021, sixteen trade associations, representing buy-side, sell-side and market infrastructures, wrote to ESMA and the European Commission regarding the timeline for implementation of the mandatory buy-in rules as part of the CSDR Settlement Discipline Regime.

The Joint Associations welcome the Report from the Commission on the CSDR Review published in July 2021 and fully support the Commission’s intention to consider amendments to the mandatory buy-in regime, subject to an impact assessment.

Related news

Policy Position

Capital Markets

CSDR

22 December 2021

Industry Approach to CSDR Settlement Discipline Regime

The Joint Associations1 welcome clarification from ESMA that national competent authorities are expected not to prioritise supervisory actions in relation to the application of the CSDR buy-in regime.2

Policy Position

Capital Markets

MIFID

15 December 2021

Joint Statement on EU Commission proposal for revised Market in Financial Instrument Regulation (MiFIR)

We see great value in the creation of a consolidated tape to support Europe’s capital markets. However, we qualify that statement with a reminder that the framework for a successful consolidated tape should

i) address the known market failure around market data costs,

Press Release

Capital Markets

MIFID

Capital Markets Union

25 November 2021

EFAMA welcomes proposal on affordable consolidated tape - The association continues to urge action on market data costs

EFAMA is pleased to read today the details of a robust MiFIR proposal from the European Commission addressing key areas of reform around the creation of a consolidated tape (CT), along with adjustments to transparency requirements on trading.

Related publications

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

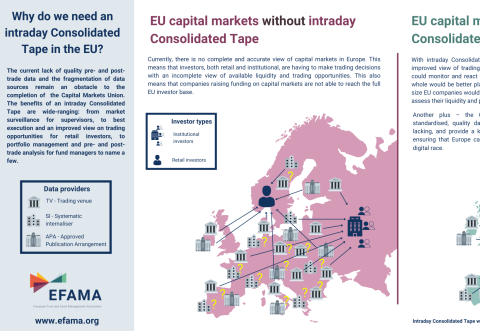

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Publication

Capital Markets

Benchmarks

06 July 2021

3 Questions to Jean-Louis Schirmann on the use of EURIBOR

Q #1 How was Euribor impacted by the adoption of the Benchmark Regulation (BMR) and what are the relevant features of the reformed Euribor for investment managers?

Publication

Capital Markets

Benchmarks

30 June 2021

3 Questions to Christophe Binet on LIBOR Transition

Q #1 When will LIBOR phase out and which rates will be replacing it?

The London Interbank Offered Rate, also known as LIBOR®, is a widely-used index for short-term interest rates that is commonly found in

Contact

Deputy Director, Capital Markets and Digital