This is a timely and necessary review to which we hope to contribute in a constructive manner. As already recognised in the consultation paper and in the MiFID Quick Fix proposal, RTS 27 and RTS 28 currently fall short of the objective of providing valuable and comparable datasets for investment managers and the investing public. We appreciate the present effort to revise reporting requirements to produce more meaningful reports.

Capital markets

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

Related policy positions

Policy position

Capital Markets

MIFID

22 December 2021

EFAMA’s response to ESMA’s Review of the MiFID II framework on best execution reports

Policy Position

Capital Markets

CSDR

22 December 2021

Industry Approach to CSDR Settlement Discipline Regime

The Joint Associations1 welcome clarification from ESMA that national competent authorities are expected not to prioritise supervisory actions in relation to the application of the CSDR buy-in regime.2

Policy Position

Capital Markets

MIFID

15 December 2021

Joint Statement on EU Commission proposal for revised Market in Financial Instrument Regulation (MiFIR)

We see great value in the creation of a consolidated tape to support Europe’s capital markets. However, we qualify that statement with a reminder that the framework for a successful consolidated tape should

i) address the known market failure around market data costs,

Related news

Press Release

Capital Markets

MIFID

30 May 2022

Cross-Industry Consensus on EU Equity Consolidated Tape

EFAMA, AFME, BVI and Cboe Europe Agree Cross-Industry Consensus on EU Equity Consolidated Tape

Monday 30 May, 2022 - AFME, BVI, Cboe Europe and EFAMA have today jointly published a position paper which provides a set of key principles needed to ensure the successful creation of an EU Equity Consolidated Tape (CT).

Policy Position

Capital Markets

MIFID

30 May 2022

EU Equity Consolidated Tape Proposal - Statement of Principles

A Cross-Industry Consensus on the EU Equity Consolidated Tape Proposal - Statement of Principles

EFAMA, AFME, BVI and Cboe agreed on a set of 11 Principles.

The provision of an appropriately constructed EU Equities Consolidated Tape (“CT”) will democratise access to equities (as proposed by the EU Commission) for all investors, regardless of resources or sophistication, with a comprehensive and standardised view of EU equities prices.

Policy Position

Capital Markets

MIFID

02 May 2022

EFAMA’s reply to ESMA’s consultation paper on the opinion on Trading Venue Perimeter

We welcome this opportunity to comment on a review of the TV perimeter, and support ESMA’s objective of clarifying when systems and facilities qualify as multilateral.

Related publications

Publication

Capital Markets

Capital Markets Union

Retail Investment

22 January 2024

Household Participation in Capital Markets

This report analyses the progress made in recent years by European households in allocating more of their financial wealth to capital market instruments (pension plans, life insurance, investment funds, debt securities and listed shares) and less in cash and bank deposits. It also includes policy recommendations on improving retail participation in capital markets, including for the Retail Investment Strategy currently under discussion.

Some key findings include:

Publication

Capital Markets

MIFID

16 November 2021

Buy-side use-cases for a real-time consolidated tape

A real-time consolidated tape, provided it is made available at a reasonable cost, will bring many benefits to European capital markets. A complete and consistent view of market-wide prices and trading volumes is necessary for any market, though this is especially true for the EU where trading is fragmented across a large number of trading venues. A real-time consolidated tape should cover equities and bonds, delivering data in ‘as close to real-time as technically possible’ after receipt of the data from the different trade venues.

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

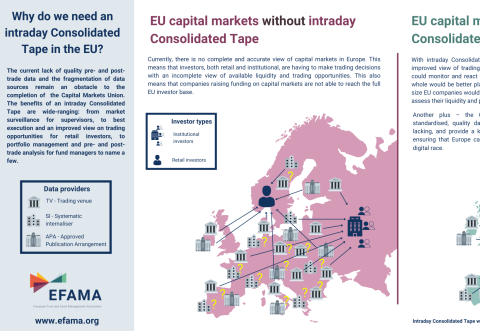

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Past events

Contact

Deputy Director, Capital Markets and Digital