MiFID / MiFIR

The Markets in Financial Instruments Directive (MiFID) is a cornerstone of EU financial services legislation and is of direct relevance to asset management companies. In 2014, the European Commission adopted new rules revising MiFID, consisting of a Directive (MiFID II) and a regulation (MiFIR). Overall, MiFID II yielded positive results in terms of liquidity and transparency for investors.

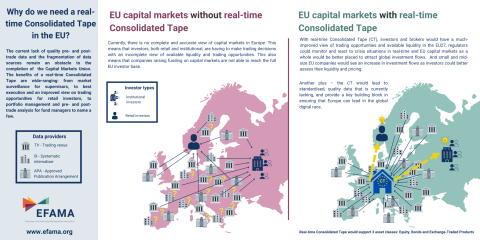

Among possible improvements to the MiFID framework, EFAMA encourages the creation of a well-structured, reasonably priced consolidated tape managed by ESMA and fed by all trading venues and systematic internalisers for all financial instruments. A second, long-term EFAMA objective is better enforcement of data providers’ existing obligation to provide market data on a “reasonable commercial basis”.

EFAMA response to ESMA's CP on MiFIR report on Systematic Internalisers in non-equity instruments

EFAMA Reply: ESMA CP on review report MiFIR transparency regime for equity, ETFs & other related instruments

Joint Statement on Market Data Costs

Reasonable Market Data Costs Benefits the Real Economy

The fundamental function of a trading venue is to match buyers and sellers of securities at a price that balances supply and demand through transparent rules and processes. The sale of market data is a related but separate by-product of that primary function.

Joint trade associations urge policymakers not to concede to suboptimal outcomes in MiFIR review

EU asset managers, banks and brokers are today urging policy makers not to concede to pressure which will lead to suboptimal outcomes in the review of the Markets in Financial Instruments Directive (MiFID/R).

European asset managers in full support of the European Parliament's proposal on Equities Consolidated Tape

In a letter to policymakers, 18 European buy-side firms state that only an Equities/ETFs tape that delivers data in real-time and that includes pre-trade data in the form of 5 layers of best bid and offer, will meet with the necessary market demand to make the Equities/ETFs Consolidated Tape commercially viable. A reasonably priced tape is also a precondition for success, they argue.

European asset managers express full support for the European Parliament’s proposal on Equities Consolidated Tape (MiFIR Review)

18 European buy-side firms, including Union, Generali, Invesco, Legal and General, Schroders and Baillie Gifford, have today declared their full support for the European Parliament’s proposal on the Equities Consolidated Tape. In a letter to policymakers, they state that only an Equities/ETFs tape that delivers data in real-time and that includes pre-trade data in the form of 5 layers of best bid and offer, will meet with the necessary market demand to make the Equities/ETFs Consolidated Tape commercially viable.