On 11 March 2021, EFAMA and 14 trade associations representing a wide range of stakeholders in the European and global financial markets wrote to the European Commission and ESMA raising concerns about the implementation of the mandatory buy-in requirement under the EU’s CSDR Settlement Discipline Regime.

Capital markets

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

Related policy positions

Policy Position

Capital Markets

CSDR

12 March 2021

Joint trade association letter regarding Implementation of CSDR SDR

Policy position

Capital Markets

MIFID

EU Fund regulation

UCITS

Management Companies

AIFMD

09 February 2021

EFAMA reply to ESMA CP on marketing communications guidelines

EFAMA believes that ESMA’s draft ‘marketing communication’ Guidelines still require important clarifications to ensure full alignment between them and MiFID II’s Commission Delegated Regulation Article 44. This alignment is essential to ensure coherent rules for fund management companies and distributors. Unfortunately, parts of the proposed Guidelines are overly prescriptive and may unintentionally make some marketing materials vaguer or even inconsistent with local MiFID requirements for distributors.

Policy position

Capital Markets

CSDR

02 February 2021

EFAMA's reply to EC's consultation on the Review of CSDR

EFAMA supports the main objectives of CSDR to increase the safety and efficiency of securities settlement, including:

- Shorter settlement periods,

- Prudential and supervisory requirements for CSDs and other institutions providing banking services ancillary to securities settlement,

- The imposition of a penalty regime under CSDR as an important step towards improving settlement efficiency in European capital markets.

Related news

Press Release

Capital Markets

02 March 2026

Deepening consolidated tape data now, rather than later, would significantly improve the competitiveness of EU capital markets

EFAMA highlights important use cases in latest publication

Policy Position

Capital Markets

08 December 2025

EFAMA response to the EBA consultation on the guidelines on the sound management of third-party risk for non-ICT related services

Press Release

Capital Markets

Capital Markets Union

Competitiveness

UCITS

Tokenisation

AIFMD

Supervision

04 December 2025

European Commission’s ambitious market integration package addresses many barriers to the Savings & Investment Union

EFAMA supports the majority of measures but warns against new ESMA supervisory reviews for large asset managers

Related publications

Publication

Capital Markets

MIFID

16 November 2021

Buy-side use-cases for a real-time consolidated tape

A real-time consolidated tape, provided it is made available at a reasonable cost, will bring many benefits to European capital markets. A complete and consistent view of market-wide prices and trading volumes is necessary for any market, though this is especially true for the EU where trading is fragmented across a large number of trading venues. A real-time consolidated tape should cover equities and bonds, delivering data in ‘as close to real-time as technically possible’ after receipt of the data from the different trade venues.

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

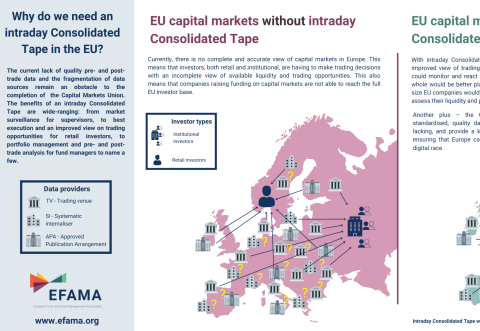

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Publication

Capital Markets

Benchmarks

06 July 2021

3 Questions to Jean-Louis Schirmann on the use of EURIBOR

Q #1 How was Euribor impacted by the adoption of the Benchmark Regulation (BMR) and what are the relevant features of the reformed Euribor for investment managers?

Past events

Members Only

EFAMA & AFME

Navigating the MiFIR Review: (Part 2) Consolidated Tape & Market Data

Virtual

Contact

Deputy Director, Capital Markets and Digital