For asset managers the main issue continues to be the reclassification of ETDs as OTCs as a result of the non-equivalence of UK regulated markets. While we understand that a review is legally mandated at this point in time, we do not see value in recalibrating the various thresholds or making changes to the calculation methodologies unless these are in the two areas we define below. Our main concern revolves around the fact that changes would carry significant compliance costs while making little impact on the population of counterparties and notional captured by the thresholds.

Capital markets

Investment managers, acting on behalf of their retail and institutional clients, are among the largest investors in financial markets. They represent a key component of the market’s “buy-side” segment.

In representing the interests of its members on wholesale capital market issues, EFAMA advocates for fair, deep, liquid, and transparent capital markets, supported by properly regulated and supervised market infrastructure.

Related policy positions

Policy position

Capital Markets

EMIR

24 January 2022

ESMA consultation on the review of clearing thresholds under EMIR

Policy position

Capital Markets

MIFID

22 December 2021

EFAMA’s response to ESMA’s Review of the MiFID II framework on best execution reports

This is a timely and necessary review to which we hope to contribute in a constructive manner. As already recognised in the consultation paper and in the MiFID Quick Fix proposal, RTS 27 and RTS 28 currently fall short of the objective of providing valuable and comparable datasets for investment managers and the investing public. We appreciate the present effort to revise reporting requirements to produce more meaningful reports.

Policy Position

Capital Markets

CSDR

22 December 2021

Industry Approach to CSDR Settlement Discipline Regime

The Joint Associations1 welcome clarification from ESMA that national competent authorities are expected not to prioritise supervisory actions in relation to the application of the CSDR buy-in regime.2

Related news

Press Release

Capital Markets

MIFID

Distribution & Client Disclosures

22 May 2020

EFAMA calls for changes to investor protection rules in MIFID II / MIFIR Review

EFAMA has submitted its  response to the European Commission's consultations on the review of the MIFID II / MIFIR regulatory framework, where it has outlined its recommendations on investor protection and capital markets and infrastructure.

response to the European Commission's consultations on the review of the MIFID II / MIFIR regulatory framework, where it has outlined its recommendations on investor protection and capital markets and infrastructure.

EFAMA's Director General Tanguy van de Werve commented:

Related publications

Publication

Capital Markets

MIFID

16 November 2021

Buy-side use-cases for a real-time consolidated tape

A real-time consolidated tape, provided it is made available at a reasonable cost, will bring many benefits to European capital markets. A complete and consistent view of market-wide prices and trading volumes is necessary for any market, though this is especially true for the EU where trading is fragmented across a large number of trading venues. A real-time consolidated tape should cover equities and bonds, delivering data in ‘as close to real-time as technically possible’ after receipt of the data from the different trade venues.

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

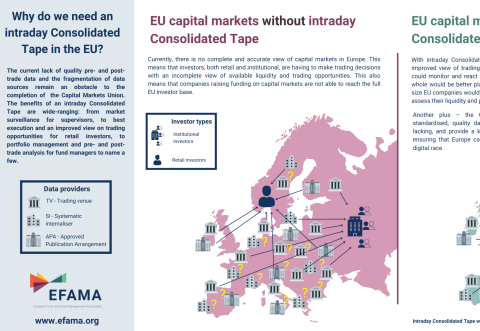

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Publication

Capital Markets

Benchmarks

06 July 2021

3 Questions to Jean-Louis Schirmann on the use of EURIBOR

Q #1 How was Euribor impacted by the adoption of the Benchmark Regulation (BMR) and what are the relevant features of the reformed Euribor for investment managers?

Contact

Deputy Director, Capital Markets and Digital