EFAMA supports the initiatives launched by IOSCO and other regulators (e.g. ESMA, FCA, SEC) to analyse and address the significant issues concerning market data in the secondary equity market.

MiFID

The Markets in Financial Instruments Directive governs how funds (and other financial instruments) can be sold and distributed to investors throughout the EU. It does this by balancing investor protection (governing under what rules and conditions investment advice and portfolio management can be given) with providing the right amount of information about products and services (information about the products’ objectives and costs). In most cases, this type of financial advice, which connects funds with end investors, is provided not by fund managers, but by other financial players, such as banks or financial advisers.

Against this backdrop, EFAMA wants to ensure that these rules are balanced and the information provided to investors is meaningful. While more protection is necessary for retail investors, MiFID should allow other, more professional investors, more freedom in defining what information is necessary to conduct their day-to-day business. Also, MiFID must not make it impossible for ordinary EU citizens to access financial advice to save for their future and retirement.

Related policy positions

Policy position

Data

International agenda

01 March 2021

EFAMA responds to IOSCO Consultation on Market Data in Secondary Equity Market

Policy position

Capital Markets

MIFID

EU Fund regulation

UCITS

Management Companies

AIFMD

09 February 2021

EFAMA reply to ESMA CP on marketing communications guidelines

EFAMA believes that ESMA’s draft ‘marketing communication’ Guidelines still require important clarifications to ensure full alignment between them and MiFID II’s Commission Delegated Regulation Article 44. This alignment is essential to ensure coherent rules for fund management companies and distributors. Unfortunately, parts of the proposed Guidelines are overly prescriptive and may unintentionally make some marketing materials vaguer or even inconsistent with local MiFID requirements for distributors.

Policy position

Data

11 January 2021

EFAMA's reply to ESMA's CP on the Guidelines on the MiFID II / MiFIR Obligations on Market Data

EFAMA welcomes this ESMA initiative and we agree with the conclusions in the ESMA Report that there is an overall need to strengthen the laws applicable to data in connection with the MiFIDII/MiFIR Review, aside the implementation of a Consolidated Tape . We consider that the draft Guidelines will further strengthen the MiFID level 1 and level 2 measures and will foster the establishment of a cost-based approach for market data procurement. Therefore, we would be in favour of turning the proposed guidelines into binding regulation.

Related news

Policy Position

Capital Markets

MIFID

07 July 2021

Ensuring a market structure and a transparency regime which facilitate liquidity, investors’ choice, and funding of companies | Joint statement

Well-functioning and liquid capital markets are fostered by an efficient market structure and supporting legislative frameworks. A diverse and efficient market structure reduces the costs of trading whilst promoting best execution. This optimises funding opportunities for issuers and maximises returns for investors and savers.

Announcement

MIFID

Competitiveness

Distribution & Client Disclosures

15 February 2021

FinDatEx launches interim version of European MiFID Template

The Financial Data Exchange Templates (FinDatEx) platform today published an interim version of the European MiFID Template (EMT V3.1) which is available on the FinDatEx website. The purpose of this interim version is to answer the demand of product distributors and manufacturers to cope with the basic implementation of MiFID II ESG/SFDR principles, and in view of the misaligned application dates of SFDR Level 1, SFDR RTS and MiFID II delegated acts.

Announcement

MIFID

Distribution & Client Disclosures

01 December 2020

Financial Data Exchange Templates (FinDatEx) platform publishes European Feedback Template

Financial Data Exchange Templates (FinDatEx) platform published on 01 December 2020 the European Feedback Template (EFT V1). This template standardises the information to be sent back from the distributor to the manufacturer under the MiFID 2 target market requirements. This is the first European wide feedback template. The EFT and all other FinDatEx templates are not compulsory, provided to the industry free of charge and are free of any intellectual property rights.

Related publications

Publication

Capital Markets

MIFID

16 November 2021

Buy-side use-cases for a real-time consolidated tape

A real-time consolidated tape, provided it is made available at a reasonable cost, will bring many benefits to European capital markets. A complete and consistent view of market-wide prices and trading volumes is necessary for any market, though this is especially true for the EU where trading is fragmented across a large number of trading venues. A real-time consolidated tape should cover equities and bonds, delivering data in ‘as close to real-time as technically possible’ after receipt of the data from the different trade venues.

Infographic

Capital Markets

MIFID

Capital Markets Union

Data

06 October 2021

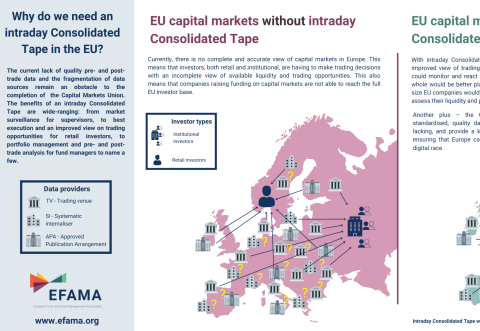

Visual | Why do we need a real-time Consolidated Tape in the EU?

The current lack of quality pre- and post-trade data and the fragmentation of data sources remain an obstacle to the completion of the Capital Markets Union. The benefits of a real-time Consolidated Tape are wide-ranging: from market surveillance for supervisors, to best execution and an improved view on trading opportunities for retail investors, to portfolio management and pre- and post-trade analysis for fund managers to name a few.

Publication

MIFID

Distribution & Client Disclosures

PRIIPs

Management Companies

AIFMD

03 June 2020

Investment Funds Distributor Due Diligence Questionnaire

Funds face unique challenges in performing intermediary oversight, and especially so because of MiFID II requirements, changing regulatory landscapes, and the absence of an industry agreed-upon standard between funds and their distribution channels. To help address these challenges, a dedicated working group developed a uniform due diligence questionnaire (DDQ) that will serve as the standard for investment funds (UCITS and AIFs) in performing onboarding and ongoing oversight of distribution channels.

Contact

Deputy Director, Regulatory Policy